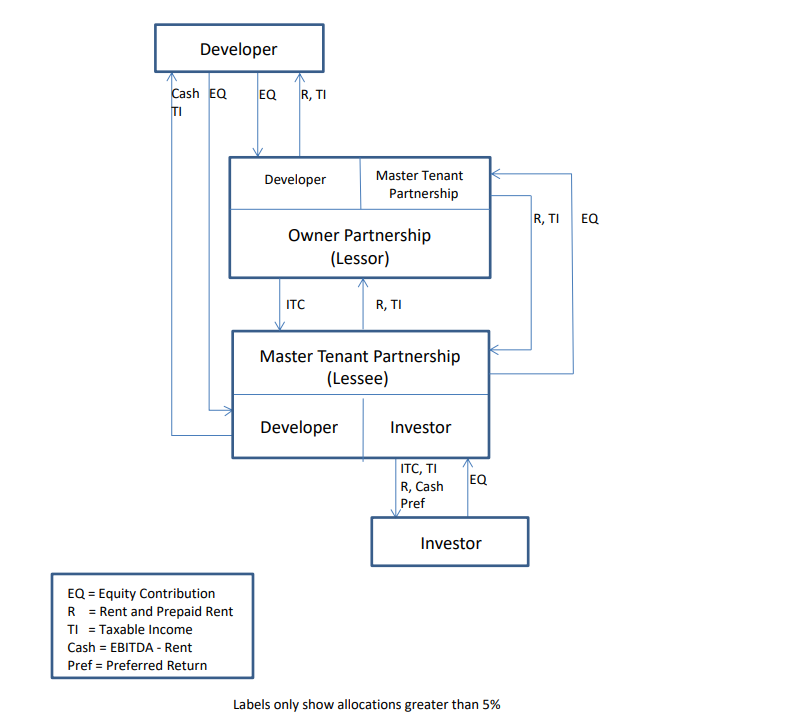

The Solar Lease Pass-Through (also called an “inverted lease”) described in a separate write-up involves two parties, a Developer who is the lessor and an Investor who is the lessee. A more complex version of this structure is a two-tier partnership arrangement that involves four entities: an Owner partnership as the lessor, a Master Tenant partnership as the lessee, an Investor who participates in the Master Tenant partnership, and a Developer who participants in both the Owner and Master Tenant partnerships.

The centerpiece of the transaction remains a lease pass-through where the Owner partnership passes the Investment Tax Credit (ITC) through to the Master Tenant partnership. The amount the Master Tenant partnership pays the Owner partnership is usually in the range of 1.2 to 1.3 times the ITC and is referred to as the credit price. At the beginning of the lease, the Master Tenant partnership makes a prepayment of rent equal to the credit price and for the remainder of the lease receives the project EBITDA, using a portion of it to pay the rent and retaining the balance. The lessee/Master Tenant may require a return on investment, usually expressed as an XIRR on the full-term pre-tax cash flows including the ITC. Typical returns are in the 2.00% to 3.00% range.

The Owner partnership participants are the Master Tenant partnership with a 49% interest and the Developer with a 51% interest. Capital contributions, cash distributions, and taxable income are all allocated in the same 49%/51% ratio. These allocations remain constant for the term of the partnership.

The Master Tenant partnership receives the ITC but does not apply basis reduction because it has no depreciable asset. Instead, the Master Tenant partnership reports 50(d) income equal to half the ITC, spread straight-line over the life of the associated asset, which is five years for solar equipment. The Owner partnership owns the asset and depreciates the full basis.

The Master Tenant partnership is a Partnership Flip structure consisting of the Investor and the Developer. The Investor’s equity contribution may be calculated to provide a required XIRR on the flipterm after-tax cash flows. Prior to the flip date the Investor receives 99% of the ITC and taxable income, a percentage of the distributable cash, and may require a preferred return on his contributed capital. After the flip date, the sharing percentages change to typically 95% of both the distributable cash and taxable income allocated to the Developer and 5% to the Investor.

The Investor receives a return as a participant in the Master Tenant partnership. After making an equity contribution, the Investor receives ITC, a preferred return, an allocation of rent from the Owner partnership, EBITDA in excess of rent from the Master Tenant partnership, and taxable income.

The Developer’s return on investment comes from both the Master Tenant and Owner partnerships. The Developer makes equity contributions to both partnerships and receives allocations of rent and taxable income from the Owner partnership and allocations of EBITDA in excess of rent and taxable income from the Master Tenant partnership.

The content provided above is intended for the informational use of our clients, and does not constitute legal or accounting advice. The material is not guaranteed to be correct, complete, or up-to-date.